Catch a high-flying fund - up 56% |

Date: Thursday, December 3, 2009

Author: Mina Kimes, CNNMoney

Now a father-and-son act, the celebrated Yacktman value portfolio has racked up big returns, showing how patience and a contrarian bent can pay off.

|

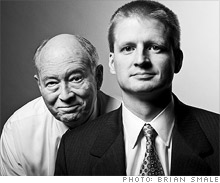

| Don Yacktman and his son, Stephen |

Back in the late-1990s tech boom, the Yacktman Fund (YACKX) lagged because he favored nontech small-cap stocks. His board tried to oust him, and investors fled. Then the dotcom bubble burst -- and Yacktman looked like a genius, topping the S&P 500 index by 34 points in 2002.

When the market started roaring again in 2003, he stuck with consumer stocks and trailed his peers for a few years. But after the market tanked last year, Yacktman, 68, who runs the fund with his son Stephen, 39, triumphed again, beating the index by 11 points in 2008. "Peak to peak, we've shown our stripes," he says.

Indeed, Yacktman's long-term record shines: The fund's 10-year annualized return of 12% ranks in the top 1% of all diversified U.S. equity funds, according to Morningstar. Among funds that invest in large-cap value stocks, Yacktman is in the top 1% for the past one, three, five, and 10 years. So far in 2009, it's up 56%, 31 points better than the S&P.

Why does the fund fly when others flail? Its managers are happy to wait -- sometimes for several years -- for bubbles to burst before scooping up what they perceive as true values. In the meantime they prefer stable, cash-generating equities, which can result in lukewarm returns when stocks are hot.

"When the market gets roaring -- that's when we have our toughest relative performance," says Don. "We're wired to buy things when they're out of favor."

That tactic has paid off during the financial crisis. At the beginning of 2008, when many value funds were gorging on financials and turnaround plays, Yacktman's top holdings were blue-chips Coca-Cola (KO, Fortune 500) and Microsoft (MSFT, Fortune 500); as of March of that year, 25% of the portfolio was in cash.

After the market crashed that autumn, the managers swooped in, snagging shares of entertainment company Liberty Media, retailer Williams-Sonoma (WSM), and subprime auto lender AmeriCredit (ACF) at steep discounts. All three stocks have since popped.

Don says his team's investing strategy is simple: "Conceptually, we think of what we do as buying bonds," meaning they focus on a company's credit quality, valuation, and future cash flows.

Recently that approach led the Yacktmans to boost their position in Pfizer (PFE, Fortune 500), which has seen its share price fall on concerns about patent expirations and health-care reform but still offers a stable cash flow and a 3.6% dividend yield. "You can get your money back there in five years," says Stephen. "Right now, you're compensated very well for what you're paying."

Ever the contrarians, the Yacktmans are also throwing their weight behind consumer staples stocks, which have lagged during this rally. Two of their biggest positions are in Coca-Cola and Pepsi (PEP, Fortune 500). Stephen says he likes the beverage makers' business models, which enable them to retain large chunks of their profits.

"The average company has to reinvest half of its earnings," he says. "When [Coke and Pepsi] earn a dollar, they get to keep 90¢." He also expects continued weakness in the dollar to boost their international profits.

The managers' riskier bets include News Corp. (NWS, Fortune 500) and Viacom (VIA.B), both top holdings that they beefed up last year. The Yacktmans view the companies as the best names in troubled industries. Stephen says it doesn't matter whether advertising bounces back soon: Both businesses' earnings are strong enough to justify their stock prices.

Similarly, he thinks cable TV provider Comcast (CMCSA, Fortune 500) is cheap, given its high free cash flow. "The primary concern there is a stupid acquisition," he says, obliquely referring to the company's anticipated buyout of NBC Universal. "But that's factored into the price."

History suggests that when the market is poised for a rebound, Yacktman's returns will start diminishing. But Stephen says many of their current holdings have room to run. "The stocks we hold now are at lower prices than they were two years ago, so our forward-return prospects are better," he says.

Morningstar analyst John Coumarianos points out that the Yacktman fund has 82% of its assets in stocks, a higher amount than usual, indicating that the managers still see value in the market.

Anyone who invests in the fund, he says, should be prepared to stay put for years -- and ride out periods of lagging returns. "The fund will look out of step at times," he says. "[But] his long-term performance is just stellar."

Don, who is accustomed to the ebb and flow of popularity, is sanguine

about the fund's surging inflows. "I've watched this happen over and over

again," he says. Stephen is more critical: "It's kind of weird how you can

outperform by 40 points, then lag by two to three points for three years,

and people will scream and yell," he says. Fair-weather investors ought to

stick around, he adds: When the next storm hits, Yacktman will prevail

again. ![]()

Reproduction in whole or in part without permission is prohibited.